Carregar apresentação

A apresentação está carregando. Por favor, espere

1

Regime de Metas para Inflação no Brasil: Construindo Credibilidade em Contexto de Volatilidade na Taxa de Câmbio André Minella Paulo S. de Freitas Ilan Goldfajn Marcelo K. Muinhos Banco Central do Brasil Julho 2003 Versão reduzida e atualizada de “Inflation Targeting in Brazil: Lessons and Challenges”

2

1. Introdução Motivação O desafio do sistema de metas para a inflação (IT) no Brasil História de alta inflação Necessidade de construção de credibilidade Ambiente de choques significativos Como balancear flexibilidade e credibilidade? There has been few option lasted for monetary policy in the world and especially for Latin American, since the adoption of fixed exchange rate is out of fashion and no one is trust more in monetary aggregate. Inflation targeting (IT) is doing well in general, although a bit less so in Latin American countries

is doing well in general, although a bit less so in Latin American countries.")

3

Panorama dos primeiros 3 anos e meio Construção de credibilidade

O trabalho examina os desafios enfrentados pelo regime de metas para inflação no Brasil ( ) Panorama dos primeiros 3 anos e meio Construção de credibilidade Função reação do Banco Central (Bacen) Expectativas de inflação e o papel das metas Mudança na dinâmica da inflação Variação da taxa de câmbio e repasse cambial para os preços This paper try to answer how Brasil has been done with the trade-off credibility& flexibity using the IT experience in the last 4 years. The big source of volatility was the confidence crise with the election outcome and the fiscal sustaintability in the last quarter of It generated a reduction in the capital inflows of 6% of the GDP and a major devaluation. Almost 50% in nominal terms. The question is how inflation targeting will rebuild the credibility of the monetary policy?

Panorama dos primeiros 3 anos e meio. Construção de credibilidade. Função reação do Banco Central (Bacen) Expectativas de inflação e o papel das metas. Mudança na dinâmica da inflação. Variação da taxa de câmbio e repasse cambial para os preços. This paper try to answer how Brasil has been done with the trade-off credibility& flexibity using the IT experience in the last 4 years. The big source of volatility was the confidence crise with the election outcome and the fiscal sustaintability in the last quarter of It generated a reduction in the capital inflows of 6% of the GDP and a major devaluation. Almost 50% in nominal terms. The question is how inflation targeting will rebuild the credibility of the monetary policy")

4

Principais resultados das estimações

Metas para inflação -> coordenador de expectativas Bacen -> reação forte diante das expectativas de inflação Grau de persistência da inflação -> redução Repasse da taxa de câmbio para IPCA: - para preços administrados é duas vezes maior do que para preços livres

5

2. Panorama de

6

Política macroeconômica

Metas para inflação Taxa de câmbio flutuante Mudança no regime fiscal

7

Mudança no regime fiscal

8

Regime IT: bem-sucedido, extremamente importante para estabilização macroeconômica

1999 e 2000: meta cumprida 2001 e 2002: meta não cumprida – diversos choques atingiram a economia

9

2001 e 2002: choques 2001 2002 Crise energética doméstica

Terroristas ataques nos EUA em 11/Set. Crise argentina 2002 Aumento da aversão ao risco nos mercados internacionais Crise de confiança: incerteza sobre a política econômica futura

10

Taxa de câmbio

11

Mudança nos preços relativos: preços administrados

O grupo inclui gasolina, gás de cozinha, eletricidade, telefone, ônibus urbano 30% do IPCA Dinâmica é diferente de outros preços: - preços internacionais - maior repasse da taxa de câmbio - maior inércia: comportamento baseado no passado é mais acentuado

12

Preço relativo entre os grupos de administrados e de livres

13

Taxa de Juros - Selic

14

Contribuições para a inflação

15

Volatilidades Pré e pós adoção do regime de metas para inflação: volatilidade de inflação, PIB, e taxa de juros After the adoption of the IT in Brazil all major variable but exchange rate showed a reduction in the volatility. The real effects of interest rate in Brazil are higher than the exchange rate, then a greater volatility of the exchange rate than interest rate is better for the growth. It is important to stress the level of GDP after the IT even more tougher international environment.

16

3. Construção de credibilidade

17

3.1. Função reação do Banco Central

Resultados: Taxa de juros responde significativamente às expectativas de inflação Política monetária Conduzida olhando para o comportamento futuro da inflação Consistente com o regime de metas para inflação where it is the Selic rate decided at the Copom meeting, yt is the output gap, Etpt+j is inflation expectations and p*t+j is the inflation target, both referring to some period in the future, as it will be explained below, and DER is the nominal exchange rate variation. The Brazilian inflation-targeting regime sets year-end inflation targets for the current and the following two years. Since it is necessary to have a single measurement of inflation deviation from the target, it was necessary to create a new variable, weighting the expected deviations from target in different years.

18

Utilizando expectativas de inflação do Banco Central

In the first one, the Selic rate decision depends only on inflation expectations and output gap. The second specification adds a term for nominal exchange rate movement. There has been a high degree of interest-rate smoothing. The coefficient on lagged interest rate is between 0.6 and 0.7. The coefficient on output gap presents the wrong sign. We have also tested for the inclusion of exchange rate change in the reaction function, but this variable is not statistically significant.

19

Utilizando expectativas de inflação dos agentes privados

In the first one, the Selic rate decision depends only on inflation expectations and output gap. The second specification adds a term for nominal exchange rate movement. There has been a high degree of interest-rate smoothing. The coefficient on lagged interest rate is between 0.6 and 0.7. The coefficient on output gap presents the wrong sign. We have also tested for the inclusion of exchange rate change in the reaction function, but this variable is not statistically significant.

20

Resultados da função reação

Expectativas de inflação: Estimativas pontuais: Expectativas de inflação do Bacen: 2,7 – 5,7 Expectativas de inflação do agentes privados: 2,0 – 2,3 (mais precisas) Todas especificações: maior do que zero Maioria das especificações: maior do que um Alto grau de suavização da taxa de juros: 0,7 – 0,9 With the sample ending in June 2002, interest rate smothing is higher (0.7) and reaction to expected inflation smaller (1,5).

Todas especificações: maior do que zero. Maioria das especificações: maior do que um. Alto grau de suavização da taxa de juros: 0,7 – 0,9. With the sample ending in June 2002, interest rate smothing is higher (0.7) and reaction to expected inflation smaller (1,5).")

21

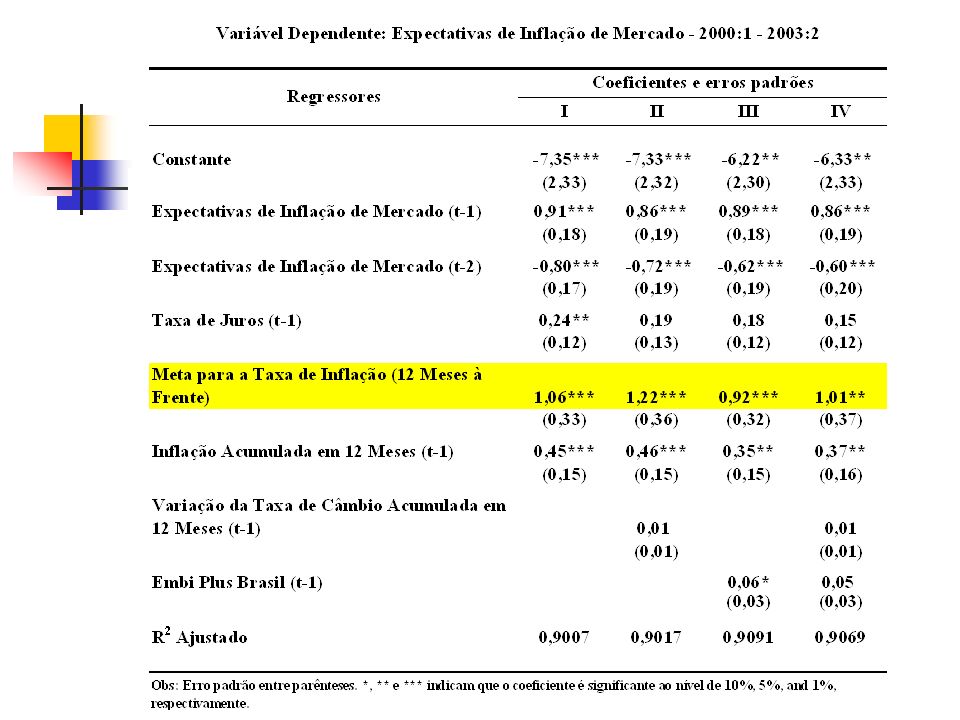

3.2. Expectativas de inflação e o papel das metas

Expectativas sob controle exigem: Conduta da política monetária consistente com o regime de metas para inflação Clara comunicação com o público

22

Expectativas e metas para inflação (12 meses à frente) e inflação nos 12 meses anteriores

As the graph shows, the gap between actual and expected inflation increased after mid-2001, when actual inflation surpassed the upper limit of the tolerance interval. Therefore, especially for this period, the credibility of the Central Bank seemed to be essential to keep inflation expectations under control. It is noteworthy that the difficulties the country faced last year impacted inflation expectations only in the last quarter of 2002. The median of inflation expectations for 2002, surveyed by the Banco Central do Brasil’s Investor Relations Group (Gerin), leveled out at around 4.5% through September, but then rapidly deteriorated afterwards and reached 11% at the end of December

, leveled out at around 4.5% through September, but then rapidly deteriorated afterwards and reached 11% at the end of December.")

24

Resultados – Expectativas de inflação dependem de:

Metas para inflação (positivamente) - > Papel das metas Taxa de juros (positivamente) -> Reação da taxa de juros a choques inflacionários Inflação passada Significativa quando a amostra termina em Fev./2003 em vez de terminar em Jun./2002

- > Papel das metas. Taxa de juros (positivamente) -> Reação da taxa de juros a choques inflacionários. Inflação passada. Significativa quando a amostra termina em Fev./2003 em vez de terminar em Jun./2002.")

25

Estimativas recursivas

26

Prevendo expectativas de inflação durante a crise de confiança?

27

Choques significativos: expectativas de inflação podem se afastar da meta mas devem reverter

28

3.3. Mudança na dinâmica da inflação

Estimação de uma curva de Phillips simples Inflação depende de: Taxa de desemprego -> significante e sinal esperado Mudança na taxa de câmbio -> significante e sinal esperado Inflação passada Mudança na dinâmica da inflação Período de IT: decréscimo no grau de persistência da inflação

30

Coeficientes variantes no tempo para o termo da inflação defasada

31

4. Variação da taxa de câmbio e repasse cambial

1999:07 – 2002:12 Média mensal de aumento: 1,8% p.m. Desvio padrão: 4,2

32

Estimativa recursiva: mudança no repasse cambial

33

Estimação de um vetor auto-regressivo (VAR)

Produto industrial Preços administrados Preços livres EMBI+ Taxa de câmbio Taxa de juros The variables used are the log-levels of output, administered prices, market prices, IPCA and exchange rate, and the levels of EMBI+ spread and interest rate. We use a Cholesky decomposition with the following order in the first specification: output, administered prices, market prices, EMBI+, exchange rate, and interest rate. In the second specification, the consumer price index substitutes for administered and market prices. Since the financial variables react more rapidly to shocks, we include them after output and price. We also estimate using interest rate before exchange rate. The results, even numerically, are very similar.

34

Funções Impulso-Resposta

The variables used are the log-levels of output, administered prices, market prices, IPCA and exchange rate, and the levels of EMBI+ spread and interest rate. We use a Cholesky decomposition with the following order in the first specification: output, administered prices, market prices, EMBI+, exchange rate, and interest rate. In the second specification, the consumer price index substitutes for administered and market prices. Since the financial variables react more rapidly to shocks, we include them after output and price. We also estimate using interest rate before exchange rate. The results, even numerically, are very similar.

35

Funções Impulso-Resposta (cont.)

The variables used are the log-levels of output, administered prices, market prices, IPCA and exchange rate, and the levels of EMBI+ spread and interest rate. We use a Cholesky decomposition with the following order in the first specification: output, administered prices, market prices, EMBI+, exchange rate, and interest rate. In the second specification, the consumer price index substitutes for administered and market prices. Since the financial variables react more rapidly to shocks, we include them after output and price. We also estimate using interest rate before exchange rate. The results, even numerically, are very similar.

36

Repasse cambial

37

Principais conclusões

Regime de metas para inflação no Brasil Importante para a obtenção de baixos níveis de inflação mesmo no contexto de choques significativos

38

Principais conclusões (cont.)

Regime enfrentou muitos desafios: 1. Construção de credibilidade Bacen tem reagido de forma consistente com o regime de metas para inflação -> olhando para o futuro Expectativas de inflação Sob controle Papel das metas Redução no grau de persistência da inflação

39

Principais conclusões (cont.)

2. Mudança nos preços relativos -> inflação 3. Mudanças na taxa de câmbio -> inflação Repasse dos preços administrados é duas vezes maior do que para os preços de mercado 4. Crise de confiança no segundo semestre de 2002

Apresentações semelhantes

e Efeitos>")